Uncertainty and Scenario Forecasting

Source:vignettes/uncertainty-and-scenarios.Rmd

uncertainty-and-scenarios.RmdOverview

bridgr can return point forecasts only, or it can also

compute coefficient uncertainty for the fitted target equation and

prediction intervals for forecasts.

The relevant estimation arguments are:

-

se = FALSE: point forecasts only. -

se = TRUE: compute HAC or Delta-HAC coefficient uncertainty and prediction intervals. -

bootstrap = list(N = 100, block_length = NULL): control the number of predictive simulation paths.block_lengthis only used whenfull_system_bootstrap = TRUE, where it sets the size of the contiguous target-period blocks resampled in each bootstrap draw — larger blocks preserve more temporal dependence. -

full_system_bootstrap = TRUE: replace the default residual-resampling prediction intervals and HAC / Delta-HAC coefficient standard errors with a full-system target-period block bootstrap. Because this refits the full mixed-frequency workflow on every draw, it can be substantially slower.

Fitting a Model with Default Uncertainty

gdp_growth <- suppressMessages(tsbox::ts_na_omit(tsbox::ts_pc(gdp)))

boot_model <- mf_model(

target = gdp_growth,

indic = baro,

indic_predict = "auto.arima",

indic_aggregators = "mean",

indic_lags = 1,

target_lags = 1,

h = 2,

se = TRUE,

bootstrap = list(N = 20, block_length = NULL)

)bridgr computes HAC standard errors for the linear

target equation, or Delta-HAC standard errors when parametric

aggregation weights are estimated jointly. Forecast uncertainty is

obtained by simulating from resampled centered residuals of the fitted

target equation.

Forecast Output

Once the model has been estimated with se = TRUE,

forecast() returns a standardized forecast object with:

meanselowerupperforecast_set- uncertainty metadata

fc <- forecast(boot_model)

fc

#> Mixed-frequency forecast

#> -----------------------------------

#> Target series: gdp_growth

#> Forecast horizon: 2

#> Uncertainty: prediction intervals from residual resampling

#> Simulation paths: 20

#> -----------------------------------

#> time mean se lower_80 upper_80 lower_95 upper_95

#> 1 2023-01-01 0.875 0.742 -0.401 1.859 -0.522 2.120

#> 2 2023-04-01 0.678 0.598 0.035 1.623 -0.317 1.970

fc$bootstrap

#> $requested

#> [1] FALSE

#>

#> $enabled

#> [1] FALSE

#>

#> $N

#> [1] 20

#>

#> $valid_N

#> [1] 0

#>

#> $block_length

#> NULLThe intervals are empirical prediction intervals based on the stored residual-resampling forecast draws.

Reporting Only Forecasts Below a Width Tolerance

In practice prediction intervals widen with horizon. A common

reporting choice is to publish only forecast horizons whose interval is

narrower than some application-specific tolerance — for example, only

publish when the 95% half-width is below a chosen threshold. The example

below applies that rule with a tolerance of 1.5 percentage

points.

forecast_table <- dplyr::tibble(

time = fc$time,

mean = as.numeric(fc$mean),

lower_95 = fc$lower[, "95%"],

upper_95 = fc$upper[, "95%"]

) |>

dplyr::mutate(

half_width_95 = (.data$upper_95 - .data$lower_95) / 2

)

tolerance <- 1.5

dplyr::filter(forecast_table, .data$half_width_95 <= tolerance)

#> # A tibble: 2 × 5

#> time mean lower_95 upper_95 half_width_95

#> <date> <dbl> <dbl> <dbl> <dbl>

#> 1 2023-01-01 0.875 -0.522 2.12 1.32

#> 2 2023-04-01 0.678 -0.317 1.97 1.14Tighten or relax tolerance depending on how much

uncertainty is acceptable in the use case.

Summary Output

The same uncertainty configuration also feeds into

summary().

summary(boot_model)

#> Mixed-frequency model summary

#> -----------------------------------

#> Target series: gdp_growth

#> Target frequency: quarter

#> Forecast horizon: 2

#> Estimation rows: 73

#> Regressors: baro, baro_lag1, gdp_growth_lag1

#> -----------------------------------

#> Target equation coefficients:

#> Estimate HAC SE

#> (Intercept) -6.249 1.424

#> baro 0.151 0.033

#> baro_lag1 -0.084 0.031

#> gdp_growth_lag1 0.012 0.073

#> -----------------------------------

#> Model fit:

#> Statistic Value

#> R-squared 0.682

#> Adjusted R-squared 0.668

#> Residual standard error 0.773

#> -----------------------------------

#> Indicator summary:

#> Frequency Predict Aggregation

#> baro month auto.arima mean

#> -----------------------------------

#> Uncertainty:

#> Coefficient SEs: hac

#> Prediction intervals: residual resampling

#> Simulation paths: 20

#> -----------------------------------The printed summary keeps the same base layout as a point-estimate model and adds the uncertainty section only when uncertainty output is available.

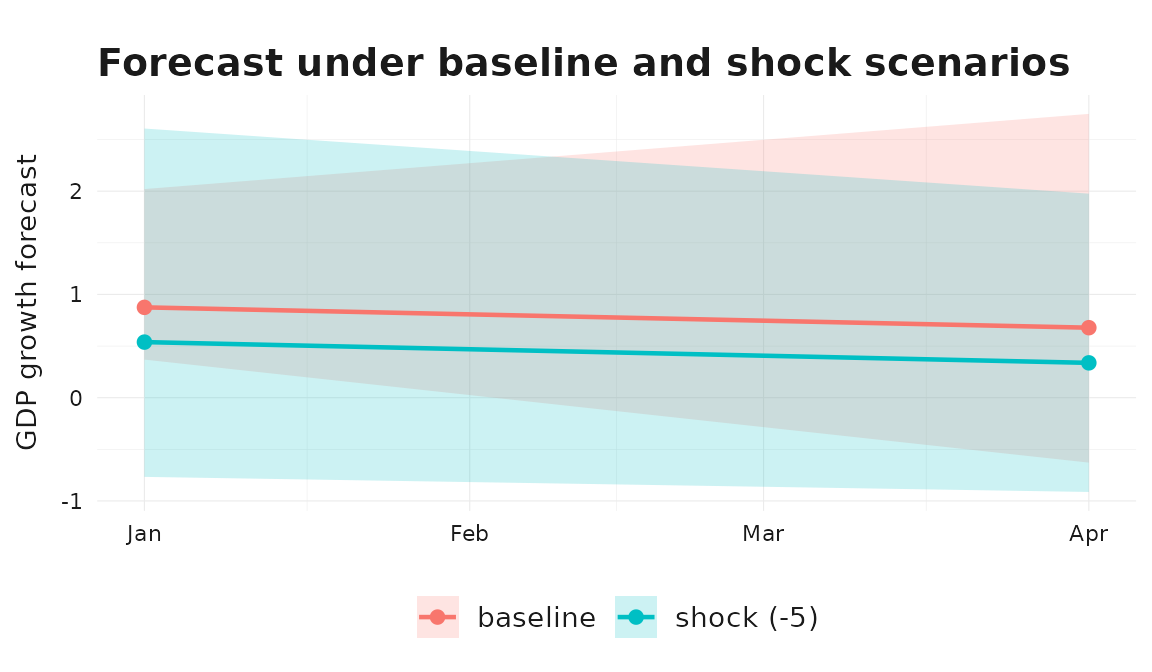

Scenario Forecasting with xreg

If you want to forecast the target under a different future regressor

path, pass a custom xreg object to forecast().

The custom regressor names must match the ones used in the fitted target

equation.

The example below defines a baseline scenario (the indicator continues on its model-implied path) and a negative shock scenario (the indicator drops by 5 points relative to baseline). Both scenarios share the fitted target equation and the same uncertainty method.

make_xreg <- function(level_shift) {

dplyr::tibble(

id = rep(boot_model$xreg_names, each = nrow(boot_model$forecast_base_set)),

time = rep(

boot_model$forecast_base_set$time,

times = length(boot_model$xreg_names)

),

value = c(

boot_model$forecast_base_set$baro + level_shift,

boot_model$forecast_base_set$baro_lag1 + level_shift

)

)

}

fc_baseline <- forecast(boot_model, xreg = make_xreg(0))

fc_shock <- forecast(boot_model, xreg = make_xreg(-5))

scenario_df <- dplyr::bind_rows(

dplyr::tibble(

scenario = "baseline",

time = fc_baseline$time,

mean = as.numeric(fc_baseline$mean),

lower = fc_baseline$lower[, "95%"],

upper = fc_baseline$upper[, "95%"]

),

dplyr::tibble(

scenario = "shock (-5)",

time = fc_shock$time,

mean = as.numeric(fc_shock$mean),

lower = fc_shock$lower[, "95%"],

upper = fc_shock$upper[, "95%"]

)

)

ggplot2::ggplot(

scenario_df,

ggplot2::aes(x = .data$time, color = .data$scenario, fill = .data$scenario)

) +

ggplot2::geom_ribbon(

ggplot2::aes(ymin = .data$lower, ymax = .data$upper),

alpha = 0.2, color = NA

) +

ggplot2::geom_line(ggplot2::aes(y = .data$mean), linewidth = 0.8) +

ggplot2::geom_point(ggplot2::aes(y = .data$mean), size = 2) +

ggplot2::labs(

title = "Forecast under baseline and shock scenarios",

x = NULL, y = "GDP growth forecast"

) +

theme_bridgr()

Scenario forecasts reuse the same uncertainty method and evaluate it on the supplied regressor path.

Optional Full-System Bootstrap

If you want to propagate uncertainty through the full mixed-frequency

workflow, including indicator completion and aggregation, set

full_system_bootstrap = TRUE. This can be substantially

slower than the default residual-resampling intervals because each

bootstrap draw re-estimates the full pipeline. In that mode, both the

reported coefficient standard errors and the forecast intervals are

based on the bootstrap draws.

full_model <- mf_model(

target = gdp_growth,

indic = baro,

indic_predict = "auto.arima",

indic_aggregators = "mean",

indic_lags = 1,

target_lags = 1,

h = 2,

se = TRUE,

full_system_bootstrap = TRUE,

bootstrap = list(N = 20, block_length = NULL)

)

forecast(full_model)$bootstrap

#> $requested

#> [1] TRUE

#>

#> $enabled

#> [1] TRUE

#>

#> $N

#> [1] 20

#>

#> $valid_N

#> [1] 20

#>

#> $block_length

#> [1] 5Point Forecasts Only

If you are only interested in point estimates, leave

se = FALSE. In that case, bootstrap is ignored

and forecast() still returns the same object shape, with

NA uncertainty fields.

point_model <- mf_model(

target = gdp_growth,

indic = baro,

indic_predict = "auto.arima",

indic_aggregators = "mean",

indic_lags = 1,

target_lags = 1,

h = 1,

se = FALSE,

bootstrap = list(N = 20)

)

forecast(point_model)

#> Mixed-frequency forecast

#> -----------------------------------

#> Target series: gdp_growth

#> Forecast horizon: 1

#> Uncertainty: point forecast only

#> -----------------------------------

#> time mean

#> 1 2023-01-01 0.875Interpretation

With the default se = TRUE, intervals are

residual-resampling prediction intervals for the fitted target equation,

and coefficient standard errors come from HAC or Delta-HAC estimation.

When full_system_bootstrap = TRUE, both the coefficient

standard errors and the forecast intervals come from a full-system block

bootstrap that resamples target-period blocks from the aligned

mixed-frequency system, refits the workflow on each draw, and evaluates

the resulting future paths.