Overview

bridgr covers classic bridge equations, MIDAS-style

mixed-frequency regressions, and intermediate specifications that

estimate within-period weights from the data, all behind a single

workflow for bridging high-frequency indicators to a

lower-frequency target.

The core workflow is always the same:

- Provide one lower-frequency target series and one or more higher-frequency indicators.

- Decide how missing indicator observations should be handled with

indic_predict. - Decide how indicators should be aligned to the target frequency with

indic_aggregators. - Fit the target equation with

mf_model(), inspect it withsummary(), and produce target-period forecasts withforecast().

This vignette walks through that workflow with the package’s built-in Swiss GDP and indicator data.

Example Data

gdp_growth <- suppressMessages(tsbox::ts_na_omit(tsbox::ts_pc(gdp)))

head(gdp_growth)

#> # A tibble: 6 × 2

#> time values

#> <date> <dbl>

#> 1 2004-04-01 0.839

#> 2 2004-07-01 -0.104

#> 3 2004-10-01 0.242

#> 4 2005-01-01 0.860

#> 5 2005-04-01 1.06

#> 6 2005-07-01 1.15

head(baro)

#> # A tibble: 6 × 2

#> time values

#> <date> <dbl>

#> 1 2004-01-01 109.

#> 2 2004-02-01 108.

#> 3 2004-03-01 109.

#> 4 2004-04-01 110.

#> 5 2004-05-01 109.

#> 6 2004-06-01 105.gdp_growth is quarterly, while baro is

monthly. mf_model() recognizes the frequency mismatch

automatically and aligns the indicator to the target frequency before

fitting the target equation.

Stationarity expectations

bridgr assumes that the series you submit are already on

a scale that is suitable for linear regression — typically growth rates,

differences, or similarly stabilized transformations. The package does

not automatically re-transform inputs, but you can enable a lightweight

pre-fit diagnostic through stationarity = "warn". The

example below shows the warning on a level GDP series and confirms that

it disappears after differencing to growth rates.

gdp_level_recent <- dplyr::slice_tail(gdp, n = 40)

baro_recent <- dplyr::slice_tail(baro, n = 120)

invisible(tryCatch(

mf_model(

target = gdp_level_recent,

indic = baro_recent,

indic_predict = "last",

indic_aggregators = "mean",

h = 1,

stationarity = "warn"

),

warning = function(w) message("Warning captured: ", conditionMessage(w))

))

#> Warning captured: Heuristic stationarity checks flagged target series `gdp_level_recent` (KPSS differencing signal). Consider differences, growth rates, log changes, demeaning, or other variance-stabilizing transformations before fitting.

stationary_model <- mf_model(

target = gdp_growth,

indic = baro,

indic_predict = "last",

indic_aggregators = "mean",

h = 1,

stationarity = "warn"

)A Basic Bridge Model

bridge_model <- mf_model(

target = gdp_growth,

indic = baro,

indic_predict = "auto.arima",

indic_aggregators = "mean",

indic_lags = 1,

target_lags = 1,

h = 2

)

forecast(bridge_model)

#> Mixed-frequency forecast

#> -----------------------------------

#> Target series: gdp_growth

#> Forecast horizon: 2

#> Uncertainty: point forecast only

#> -----------------------------------

#> time mean

#> 1 2023-01-01 0.875

#> 2 2023-04-01 0.678The default "mean" aggregator is the classic

bridge-model setup: each monthly block is completed first, then averaged

to the quarterly frequency before the target equation is estimated.

The fitted object stores the aligned data that went into estimation and the future target-period regressor path used for forecasting.

tail(bridge_model$estimation_set)

#> # A tibble: 6 × 5

#> time gdp_growth baro baro_lag1 gdp_growth_lag1

#> <date> <dbl> <dbl> <dbl> <dbl>

#> 1 2021-07-01 2.34 112. 125. 2.47

#> 2 2021-10-01 0.411 104. 112. 2.34

#> 3 2022-01-01 0.105 97.4 104. 0.411

#> 4 2022-04-01 1.03 94.3 97.4 0.105

#> 5 2022-07-01 0.255 90.0 94.3 1.03

#> 6 2022-10-01 0.102 90.7 90.0 0.255

bridge_model$forecast_set

#> # A tibble: 2 × 4

#> time baro baro_lag1 gdp_growth_lag1

#> <date> <dbl> <dbl> <list>

#> 1 2023-01-01 97.4 90.7 <dbl [1]>

#> 2 2023-04-01 99.8 97.4 <dbl [1]>Lags in the target equation

target_lags = p adds p autoregressive lags

of the target to the right-hand side of the regression.

indic_lags = q adds q lags of each

aggregated indicator (after frequency alignment). Both default to

0. In the example above the target equation is

\[ \Delta y_t = \alpha + \rho \, \Delta y_{t-1} + \beta_0 \, \bar{x}_t + \beta_1 \, \bar{x}_{t-1} + \varepsilon_t, \]

where \(\bar{x}_t\) is the within-quarter mean of the monthly indicator. Forecasts beyond the first horizon are produced recursively, with simulated target lags taking the place of observed ones once the in-sample history is exhausted.

Standardized Output

summary() and forecast() use a stable

package-specific layout. The base output is the same across bridge,

mixed-frequency, and direct-alignment specifications. Additional

details, such as optimization summaries or uncertainty settings, are

appended only when they are relevant.

summary(bridge_model)

#> Mixed-frequency model summary

#> -----------------------------------

#> Target series: gdp_growth

#> Target frequency: quarter

#> Forecast horizon: 2

#> Estimation rows: 73

#> Regressors: baro, baro_lag1, gdp_growth_lag1

#> -----------------------------------

#> Target equation coefficients:

#> Estimate

#> (Intercept) -6.249

#> baro 0.151

#> baro_lag1 -0.084

#> gdp_growth_lag1 0.012

#> -----------------------------------

#> Model fit:

#> Statistic Value

#> R-squared 0.682

#> Adjusted R-squared 0.668

#> Residual standard error 0.773

#> -----------------------------------

#> Indicator summary:

#> Frequency Predict Aggregation

#> baro month auto.arima mean

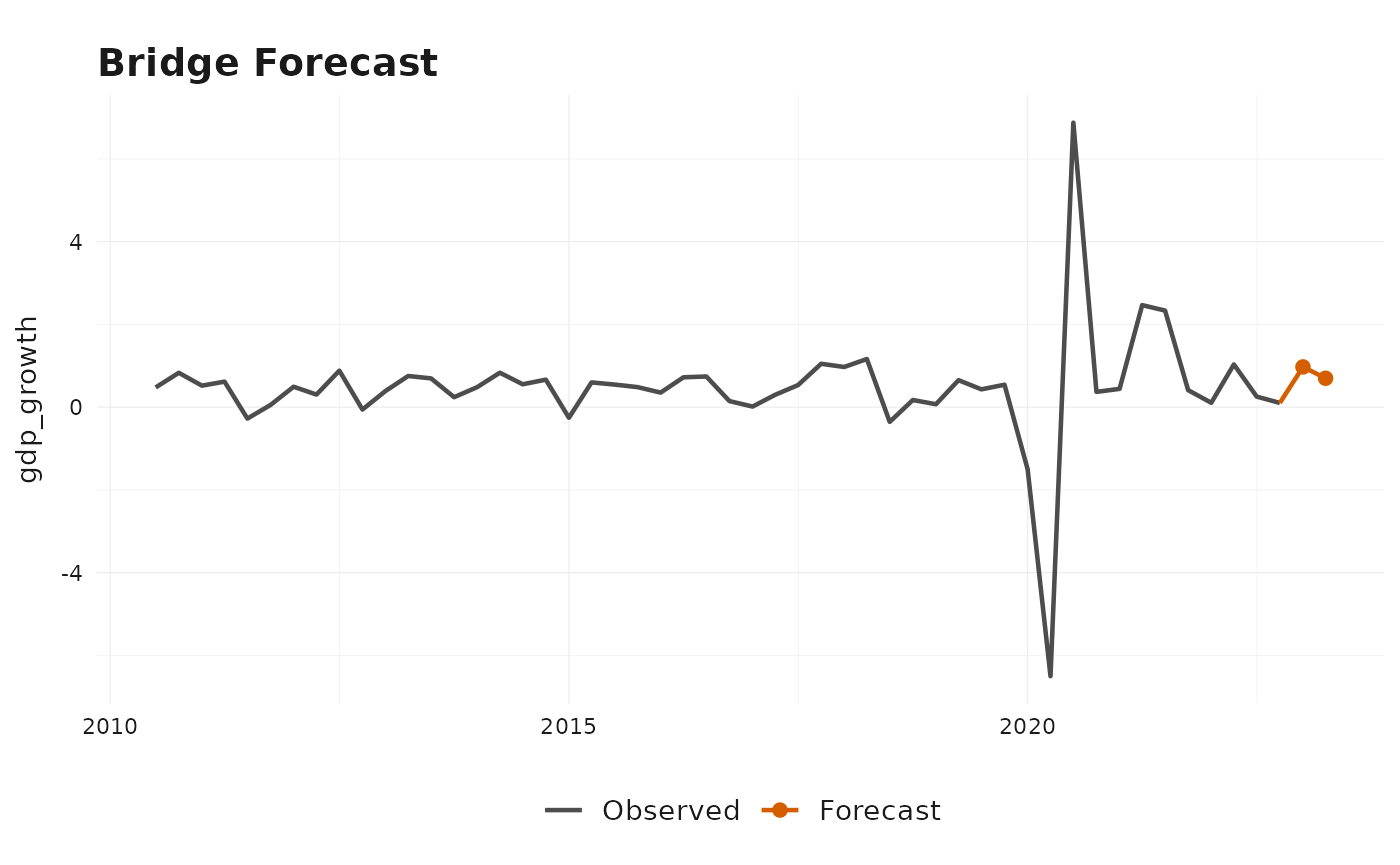

#> -----------------------------------Forecast Visualization

The package also provides a built-in plotting method for fitted

mixed-frequency models. With type = "forecast", it shows

the observed target history together with the forecast path generated by

the model.

plot(bridge_model, type = "forecast")

Multiple Indicators

mf_model() accepts any number of indicators in a single

long-format table. Indicators may share a frequency or come from

different frequencies, in which case each one is aligned to the target

separately. The example below pairs the level of the KOF barometer with

its year-over-year change as two monthly indicators.

baro_yoy <- baro |>

dplyr::arrange(time) |>

dplyr::mutate(values = values - dplyr::lag(values, 12)) |>

dplyr::filter(!is.na(values))

indic_multi <- dplyr::bind_rows(

dplyr::mutate(baro, id = "baro_level"),

dplyr::mutate(baro_yoy, id = "baro_yoy")

) |>

dplyr::select(id, time, values)

multi_model <- mf_model(

target = gdp_growth,

indic = indic_multi,

indic_predict = c("last", "last"),

indic_aggregators = c("mean", "mean"),

target_lags = 1,

h = 1

)

multi_model$regressor_names

#> [1] "baro_level" "baro_yoy" "gdp_growth_lag1"

forecast(multi_model)

#> Mixed-frequency forecast

#> -----------------------------------

#> Target series: gdp_growth

#> Forecast horizon: 1

#> Uncertainty: point forecast only

#> -----------------------------------

#> time mean

#> 1 2023-01-01 -0.324Both indicators are aggregated independently and enter the final target equation as separate regressors.

Direct Alignment

If you set indic_predict = "direct", bridgr

switches from indicator forecasting to direct alignment based only on

observed complete high-frequency blocks. In that case, the latest

complete blocks are assigned backward to target periods instead of being

forecast forward first, and they are averaged within each target

period.

direct_model <- mf_model(

target = gdp_growth,

indic = baro,

indic_predict = "direct",

h = 1

)

forecast(direct_model)

#> Mixed-frequency forecast

#> -----------------------------------

#> Target series: gdp_growth

#> Forecast horizon: 1

#> Uncertainty: point forecast only

#> -----------------------------------

#> time mean

#> 1 2023-01-01 -0.497This is particularly useful at the ragged edge when you want to work only with observed high-frequency information and avoid a separate indicator forecasting step.

Non-Standard Calendars

By default the package uses a regular frequency ladder

(second → minute → hour →

day → week → month →

quarter → year) with conventional conversion

factors such as 60 seconds per minute, 24 hours per day, and 3 months

per quarter. If your data follow a non-standard calendar — for example a

5-day business week or 50 working weeks per year — pass a named numeric

vector to frequency_conversions to override the defaults.

See ?mf_model for the full set of recognized names.

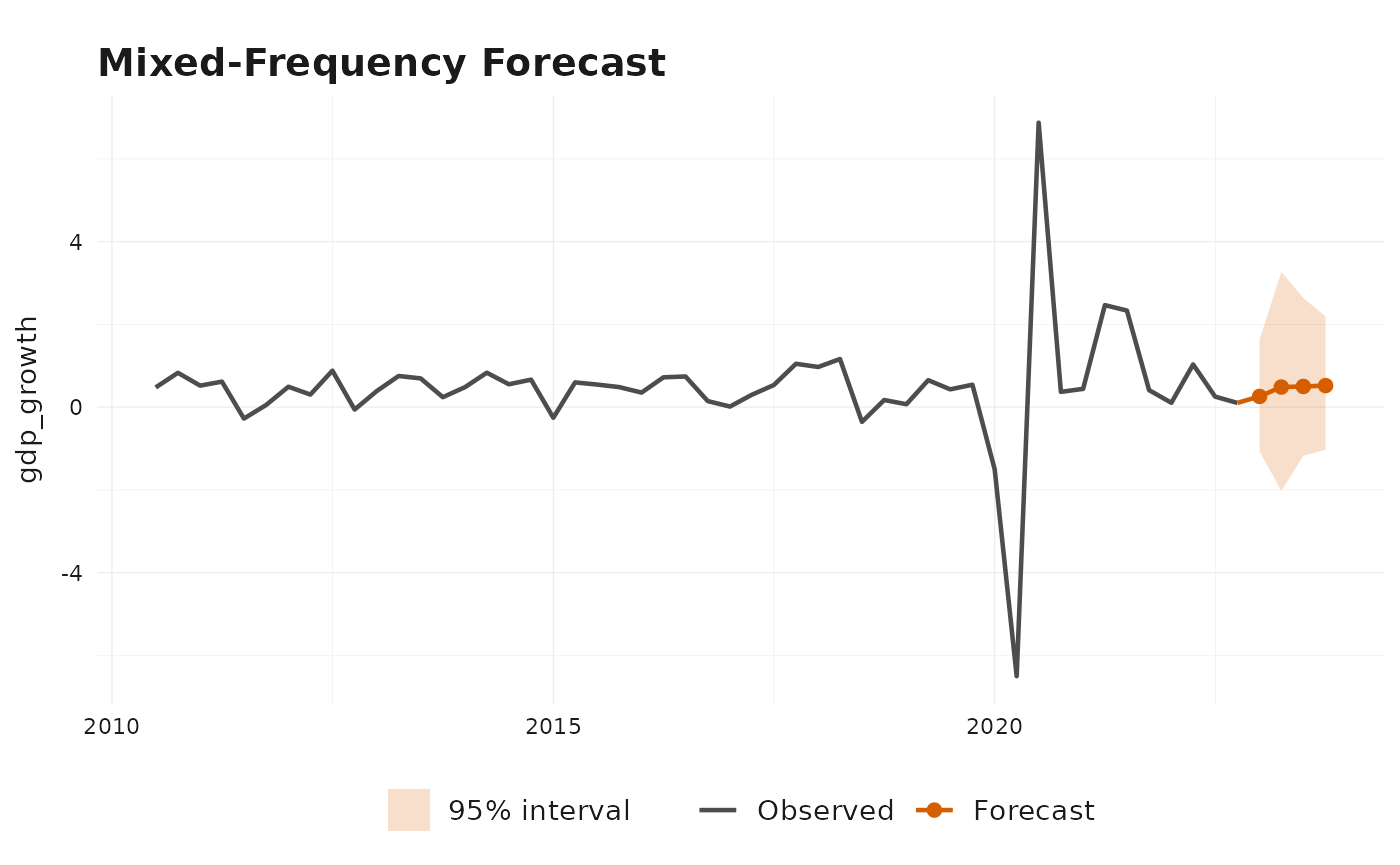

Optional Uncertainty Output

By default, bridgr returns point forecasts only. If you

want uncertainty output, request it at estimation time with

se = TRUE and, if needed, custom simulation or full-system

bootstrap controls through bootstrap.

uncertainty_model <- mf_model(

target = gdp_growth,

indic = baro,

indic_predict = "auto.arima",

indic_aggregators = "mean",

target_lags = 1,

h = 4,

se = TRUE,

bootstrap = list(N = 40, block_length = NULL)

)

forecast(uncertainty_model)

#> Mixed-frequency forecast

#> -----------------------------------

#> Target series: gdp_growth

#> Forecast horizon: 4

#> Uncertainty: prediction intervals from residual resampling

#> Simulation paths: 40

#> -----------------------------------

#> time mean se lower_80 upper_80 lower_95 upper_95

#> 1 2023-01-01 0.259 0.742 -0.804 0.975 -1.085 2.423

#> 2 2023-04-01 0.486 0.788 -0.593 1.750 -0.891 1.939

#> 3 2023-07-01 0.500 0.784 -0.601 1.422 -0.961 2.522

#> 4 2023-10-01 0.521 0.865 -0.579 1.626 -0.838 2.742

summary(uncertainty_model)

#> Mixed-frequency model summary

#> -----------------------------------

#> Target series: gdp_growth

#> Target frequency: quarter

#> Forecast horizon: 4

#> Estimation rows: 74

#> Regressors: baro, gdp_growth_lag1

#> -----------------------------------

#> Target equation coefficients:

#> Estimate HAC SE

#> (Intercept) -10.988 3.304

#> baro 0.116 0.033

#> gdp_growth_lag1 -0.316 0.120

#> -----------------------------------

#> Model fit:

#> Statistic Value

#> R-squared 0.572

#> Adjusted R-squared 0.560

#> Residual standard error 0.886

#> -----------------------------------

#> Indicator summary:

#> Frequency Predict Aggregation

#> baro month auto.arima mean

#> -----------------------------------

#> Uncertainty:

#> Coefficient SEs: hac

#> Prediction intervals: residual resampling

#> Simulation paths: 40

#> -----------------------------------

plot(uncertainty_model, type = "forecast")

The uncertainty implementation uses HAC standard errors for the

linear target equation, or Delta-HAC standard errors when parametric

aggregation weights are estimated jointly. By default, prediction

intervals are simulated from resampled centered target-equation

residuals. If you also set full_system_bootstrap = TRUE,

bridgr instead uses a full-system target-period block

bootstrap for both coefficient standard errors and prediction intervals,

controlled through

bootstrap = list(N = ..., block_length = ...).

Where to Go Next

The vignette

vignette("mixed-frequency-modeling", package = "bridgr")

compares the main aggregation strategies and shows how

bridgr moves from classic bridge models to unrestricted and

parametric MIDAS-style specifications.

The vignette

vignette("ragged-edge-nowcasting", package = "bridgr")

focuses on indic_predict and the different ways to handle

incomplete high-frequency data at the forecast origin.

The vignette

vignette("uncertainty-and-scenarios", package = "bridgr")

shows how to work with HAC / Delta-HAC coefficient uncertainty,

residual-resampling prediction intervals, the optional full-system

bootstrap, and scenario forecasts based on custom future regressor

paths.