Forecasting Swiss GDP Growth after the SNB abandoned the exchange rate floor

“The only function of economic forecasting is to make astrology look respectable.” 1

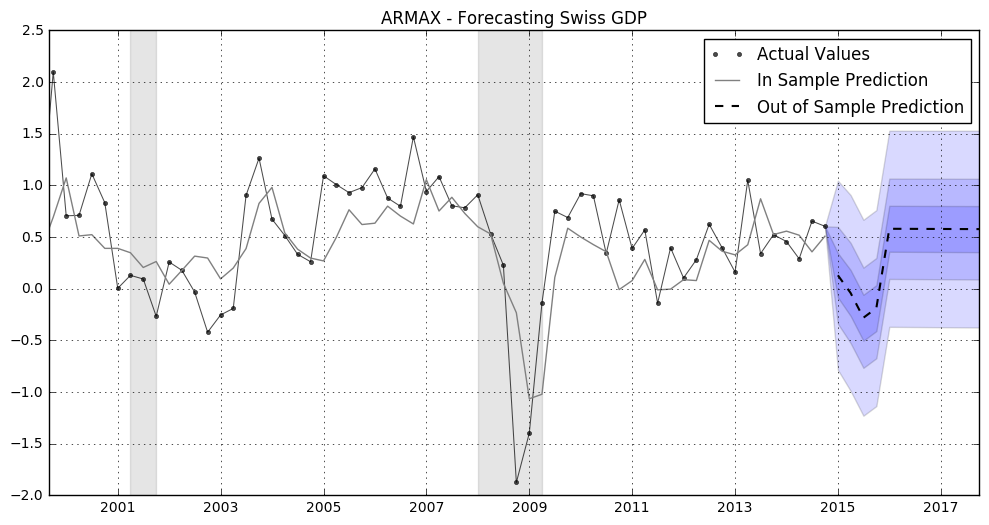

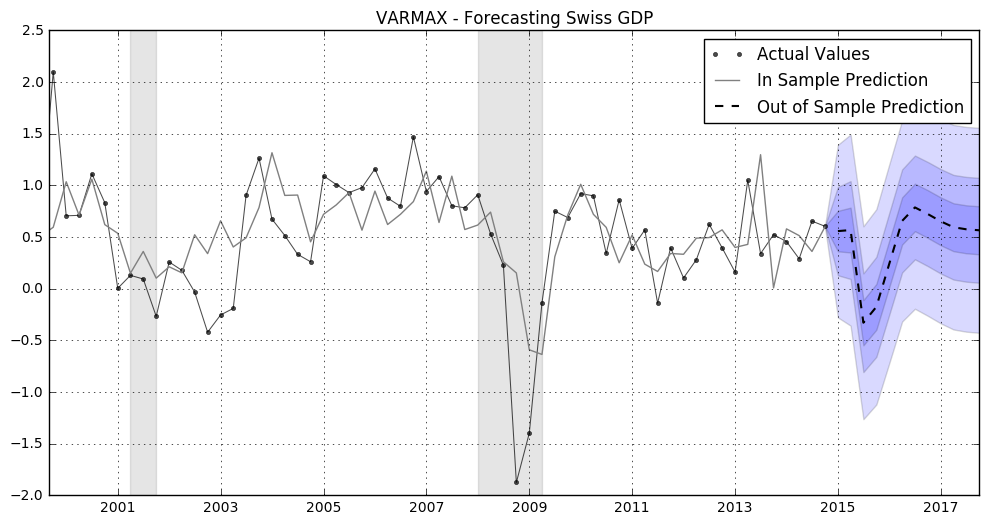

Since economic output represents the aggregated activity of many agents, influenced by forces seen and unseen, it is a wonder forecasters ever get it right. Nevertheless, I try to forecast Swiss GDP growth after an appreciation of 15% of the CHF vis-à-vis the EUR as it was the case when the SNB repealed the minimum rate.2 To do this, I use an ARMAX and a VARMAX model. The models predict considerably lower GDP growth which confirms that the models reflect the negative relationship between GDP growth and the exchange rate. Hence, both types of models exhibit quite reasonable predictive power.

To estimate the models, I use the SARIMAX and the VARMAX routines of Statsmodels. The data used can be found on the database of the St. Louis Fred and the OECD. The VARMAX model contains Swiss GDP growth, inflation, unemployment rate, exports growth, a shorter and a longer yield spread. Lagged GDP of the Euro Area and lagged CHF/EUR exchangerate build the exogenous data block. Granger Causality tests show that from a statistically point of view it’s justified to treat the exchange rate as exogenous which is an assumption that is often used when forecasting GDP growth in a small open economy, although it does not make a lot of sense economically. Economically it can reasonably be assumed, however, that Euro Area GDP growth is exogenous to Swiss GDP growth because Switzerland is a small open economy and thus is unlikely to affect GDP growth in the EU.

import numpy as np

import pandas as pd

import statsmodels.api as sm

from pandas.io.data import DataReader

import matplotlib.pyplot as plt

import warnings

warnings.simplefilter('ignore')/anaconda/lib/python3.5/site-packages/pandas/io/data.py:35: FutureWarning: The pandas.io.data module is moved to a separate package (pandas-datareader) and will be removed from pandas in a future version. After installing the pandas-datareader package (https://github.com/pydata/pandas-datareader), you can change the import ``from pandas.io import data, wb`` to ``from pandas_datareader import data, wb``. FutureWarning)

table = pd.read_excel('forecasting_data.xlsx')

idx = table.observation_date

data = table[['SwissGDP','Inflation','Unemployment','Exports','Shortspread','Longspread']]

data.index=idx

xdata = table[['EUR/CHF','EUR/CHF_L1','EUR/CHF_L2','EUR/CHF_L3','EuroGDP_L1']]

xdata.index=idx

SwissGDP = data[['SwissGDP']]

fig1 = plt.figure(figsize=(8,5))

ax1 = fig1.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(SwissGDP, lags=6, ax=ax1)

ax2 = fig1.add_subplot(212)

fig1 = sm.graphics.tsa.plot_pacf(SwissGDP, lags=6, ax=ax2)

plt.show(fig1)

The figure above shows the ACF and the PACF of Swiss GDP growth. The ACF is significantly different from zero up to two lags while the PACF is only significantly different from zero for lag one. Therefore, p = 4 and q = 4 should be according to Box and Jenkins (1976) an appropriate maximum order for the ARMAX(p,q) model. In an automated procedure several information criteria are calculated to trade-off explanatory power with parsimony.

aic = pd.DataFrame(np.zeros((5,5), dtype=float))

bic = pd.DataFrame(np.zeros((5,5), dtype=float))

# Iterate over all ARMA(p,q) models with p,q in [0,]

for p in range(5):

for q in range(5):

if p == 0 and q == 0:

continue

# Estimate the model with no missing datapoints

mod = sm.tsa.statespace.SARIMAX(SwissGDP, xdata, order=(p,0,q), enforce_invertibility=True)

try:

res = mod.fit(maxiter=5000, disp = False)

aic.iloc[p,q] = res.aic

bic.iloc[p,q] = res.bic

except:

aic.iloc[p,q] = np.nan

bic.iloc[p,q] = np.nan

aic.iloc[0,0] = np.nan

bic.iloc[0,0] = np.nan

print(aic)

print(bic)

q = aic.min().idxmin()

p = aic.idxmin()[q]

0 1 2 3 4

0 NaN 264.613956 265.895288 263.718360 265.311417

1 262.245898 255.756811 251.495686 255.245270 257.234556

2 262.613856 NaN NaN 255.466728 256.541741

3 261.917222 263.947968 NaN NaN NaN

4 263.823613 265.827257 NaN NaN NaN

0 1 2 3 4

0 NaN 285.155274 289.371079 290.128625 294.656156

1 282.787215 279.232602 277.905952 284.590009 289.513770

2 286.089647 NaN NaN 287.745941 291.755428

3 288.327487 293.292707 NaN NaN NaN

4 293.168352 298.106470 NaN NaN NaN

The AIC and the BIC are both minimized for \(p = 1\) and \(q = 2\), therefore an ARMAX(1,2) model is used here.

ARMA model

Due to Wold (1938), a covariance-stationary equation can be written as the so-called “Wold-Decomposition”:

\[\begin{aligned} Y_t = \mu + \sum_{j=0}^{\infty} \psi_j \epsilon_{t-j} \end{aligned}\]where \(\epsilon_t\) is the error from forecasting \(Y_t\) solely with lagged values of \(Y_t\). A Wold representation in principle requires fitting an infinite number of parameters (\(\psi_1, \psi_2, ...\)). With a finite number of observations this will never be possible. However, in practice a typical assumption is that \(Y_t\) is a causal process and \(\psi(L)\) can be approximated from its causal representation:

\[\begin{aligned} \sum_{j=0}^\infty \psi_j L^j = \frac{\Theta(L)}{\Phi(L)} \equiv \frac{(1 + \theta_1L + \theta_2L^2 + ... + \theta_qL^q)}{(1 - \phi_1L - \phi_2L^2 - ... - \phi_pL^p)} \end{aligned}\]ARMA modelling seeks a finite parameter approximation to the Wold representation. Box and Jenkins (1976) emphasise parsimony in the choice of the AR order \(p\) and the MA \(q\) order

The general ARMA model is:

\[\begin{aligned} Y_t = \sum_{i=0}^p \phi_i Y_{t-i} + \epsilon_t + \sum_{j=0}^q \theta_j \epsilon_{t-j} \end{aligned}\]where \(\epsilon_t\) is a disturbance term(white noise) and \(Y_t\) is the stationary forecast variable. The typical strategy implies:

- Select an appropriate maximum \(p, q\) order for the ARMA (p, q) model.

- Estimate \(\phi(L)\) and \(\theta(L)\) associated with each choice of \(p\) and \(q\).

- Select the best model (choice of \(p\) and \(q\)) based on model diagnostics.

# Statespace

mod = sm.tsa.statespace.SARIMAX(SwissGDP, xdata, order=(p,0,q))

res = mod.fit(maxiter=5000)

fig2 = res.plot_diagnostics()

print(res.summary())

plt.show(fig2)

Statespace Model Results

==============================================================================

Dep. Variable: SwissGDP No. Observations: 139

Model: SARIMAX(1, 0, 2) Log Likelihood -116.748

Date: Thu, 05 Jan 2017 AIC 251.496

Time: 17:11:42 BIC 277.906

Sample: 04-01-1980 HQIC 262.228

- 10-01-2014

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

EUR/CHF 0.0316 0.021 1.535 0.125 -0.009 0.072

EUR/CHF_L1 0.0415 0.026 1.609 0.108 -0.009 0.092

EUR/CHF_L2 0.0575 0.026 2.194 0.028 0.006 0.109

EUR/CHF_L3 0.0512 0.020 2.589 0.010 0.012 0.090

EuroGDP_L1 0.3566 0.095 3.740 0.000 0.170 0.544

ar.L1 0.9989 0.004 272.166 0.000 0.992 1.006

ma.L1 -0.7317 0.096 -7.607 0.000 -0.920 -0.543

ma.L2 -0.2350 0.093 -2.529 0.011 -0.417 -0.053

sigma2 0.3097 0.035 8.910 0.000 0.242 0.378

===================================================================================

Ljung-Box (Q): 30.26 Jarque-Bera (JB): 34.75

Prob(Q): 0.87 Prob(JB): 0.00

Heteroskedasticity (H): 0.45 Skew: -0.01

Prob(H) (two-sided): 0.01 Kurtosis: 5.45

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

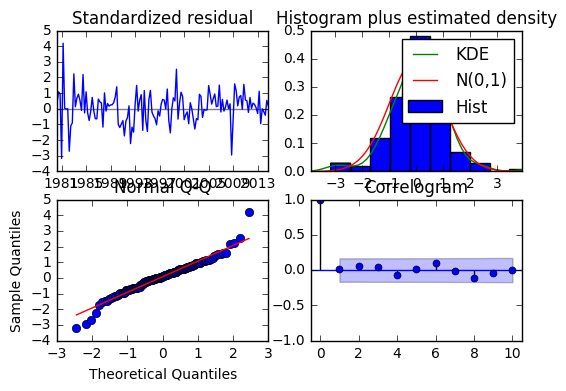

The residual plot suggest that the ARMA model fits pretty well. The fitted values track the actual values and even cover the recession during the financial crisis. The residuals look reasonably independent and identically distributed according to the ACF and also resemble a normal distribution. By looking at the ACF of the residuals it’s observable that there are no lags which are autocorrelated.

Next, the exogenous variables for the forecasting task are generated. For simplicity, I assume that the exchange rate decreases by 15% in 2015Q1 (due to the decision of the SNB to repeal the euro minimum rate on January 15) and is zero otherwise. The lagged Euro Area GDP is set to it’s mean. Then the model is used to forecast 12 quarters ahead.

# Generate Exogenous Data for Forecasting

fx = pd.DataFrame(index=list(range(0, 12)) , columns=xdata.columns)

fx = fx.fillna(0)

fx.iloc[0,0] = -15.00

fx.iloc[1,1] = -15.00

fx.iloc[2,2] = -15.00

fx.iloc[3,3] = -15.00

fx.iloc[0:12,4] = np.mean(xdata[['EuroGDP_L1']]).values# In-sample one-step-ahead predictions, and out-of-sample forecasts

nforecast = 11

predict = res.get_prediction(end=mod.nobs + nforecast, exog = fx)

""" idx = np.arange(len(predict.predicted_mean)) """

predict_ci90 = predict.conf_int(alpha=0.1)

predict_ci60 = predict.conf_int(alpha=0.4)

predict_ci30 = predict.conf_int(alpha=0.7)

fidx = predict_ci90.index

predict_ci90.iloc[138,:] = SwissGDP.iloc[138,:].values

predict_ci60.iloc[138,:] = SwissGDP.iloc[138,:].values

predict_ci30.iloc[138,:] = SwissGDP.iloc[138,:].values

# Graph

fig3, ax = plt.subplots(figsize=(12,6))

ax.grid()

ax.plot(idx,SwissGDP,'k',label='', alpha=0.7, linewidth=0.75)

ax.plot(idx,SwissGDP,'k.', label='Actual Values', alpha=0.7, linewidth=0.75)

# Plot

ax.plot( predict.predicted_mean[:-nforecast-1], 'gray',label='In Sample Prediction')

ax.plot(fidx[-nforecast-1:], predict.predicted_mean[-nforecast-1:], 'k--', linestyle='--', linewidth=1.5,label='Out of Sample Prediction')

ax.fill_between(fidx[-nforecast-2:], predict_ci90.iloc[-nforecast-2:, 0], predict_ci90.iloc[-nforecast-2:, 1], alpha=0.15, label= '')

ax.fill_between(fidx[-nforecast-2:], predict_ci60.iloc[-nforecast-2:, 0], predict_ci60.iloc[-nforecast-2:, 1], alpha=0.15, label= '')

ax.fill_between(fidx[-nforecast-2:], predict_ci30.iloc[-nforecast-2:, 0], predict_ci30.iloc[-nforecast-2:, 1], alpha=0.15, label= '')

# Retrieve and also plot the NBER recession indicators

rec = DataReader('USREC', 'fred', start=idx[0], end=idx[138])

recr = rec.iloc[0:413:3,0]

ylim = ax.get_ylim()

ax.fill_between(recr.index, ylim[0], ylim[1], recr, facecolor='k', alpha=0.1);

ax.legend()

ax.set_xlim(730000.0, 736603.0)

ax.set(title='ARMAX - Forecasting Swiss GDP');

plt.show(fig3)

We see this scenario predicts Swiss GDP to be considerably lower because of the appreciation. This reflects the positive relationship between a depreciation and GDP growth. Therefore, an appreciation of the swiss franc vis-à-vis the euro leads to lower Swiss GDP growth.

VAR model

A VAR(p) process in reduced form is:

\[\begin{aligned} y_t = c + \Phi_1y_{t-1} + ... + \Phi_py_{t-p} + \epsilon_t \end{aligned}\]Here \(y_t\) represents a set of variables collected in a vector, c denotes a vector of constants, \(\Phi_j\) a matrix of autoregressive coefficients and \(\epsilon_t\) is white noise. Since the parameters of \(\Phi_j\) are unknown, we have to estimate these parameters. To do so, the VAR can be represented in companion form:

\[\begin{aligned} Y &= (y_1, y_2, ... , y_T) \\[2em] B &= (c, \Phi_1, \Phi_2, ... , \Phi_p) \\[2em] Z &= \left[\begin{array}{cccc} 1 & 1 & ... & 1 \\ y_{0} & y_1 & ... & y_{T-1} \\ \vdots & \vdots & \ddots & \vdots \\ y_{-p+1} & y_{-p+2} & ... & y_{T-p} \end{array} \right] \\[3em] U &= (\epsilon_1, \epsilon_2, ... , \epsilon_T) \end{aligned}\]The VAR(p) can now be written compactly as

\[\begin{aligned} Y = BZ + U \end{aligned}\]and coefficients can easily be estimated via OLS or Maximum Likelihood.

# Iterate over all VARMAX(p,q) models with p,q in [0,]

for p in range(5):

for q in range(5):

if p == 0 and q == 0:

continue

# Estimate the model with no missing datapoints

mod = sm.tsa.VARMAX(data, xdata, order=(p,q), enforce_invertibility=True)

try:

res = mod.fit(maxiter=100, disp = False)

aic.iloc[p,q] = res.aic

bic.iloc[p,q] = res.bic

except:

aic.iloc[p,q] = np.nan

bic.iloc[p,q] = np.nan

aic.iloc[0,0] = np.nan

bic.iloc[0,0] = np.nan

print(aic)

print(bic)

q = aic.min().idxmin()

p = aic.idxmin()[q]

0 1 2 3 4

0 NaN 2327.172822 2268.377277 2268.557987 2184.283078

1 1738.137507 1671.993551 1703.809500 1755.831867 1725.441905

2 1595.173709 1697.197868 1720.744466 1837.434508 1814.274102

3 1691.637533 1675.031941 1755.366443 1863.706566 1953.631488

4 1709.367598 1702.215088 1805.406073 1898.357519 1983.406628

0 1 2 3 4

0 NaN 2600.078897 2646.924414 2752.746186 2774.112339

1 2011.043582 2050.540689 2187.997699 2345.661128 2420.912227

2 1973.720847 2181.386067 2310.573727 2532.904830 2615.385485

3 2175.825732 2264.861201 2450.836765 2664.817950 2860.383933

4 2299.196858 2397.685410 2606.517457 2805.109964 2995.800135

Both information criteria are minimized within the VARMAX(2,0) model.

# Statespace

mod = sm.tsa.VARMAX(data, xdata, order=(p,q), enforce_invertibility=True)

res = mod.fit(maxiter=5000, disp = False)

fig4 = res.plot_diagnostics(0)

print(res.summary())

plt.show(fig4)Statespace Model Results ============================================================================================================================================= Dep. Variable: ['SwissGDP', 'Inflation', 'Unemployment', 'Exports', 'Shortspread', 'Longspread'] No. Observations: 139 Model: VARX(2) Log Likelihood -666.505 + intercept AIC 1591.009 Date: Mon, 09 Jan 2017 BIC 1969.556 Time: 23:08:04 HQIC 1744.841 Sample: 04-01-1980 - 10-01-2014 Covariance Type: opg ================================================================================================================================= Ljung-Box (Q): 33.70, 98.21, 41.30, 35.91, 34.08, 103.01 Jarque-Bera (JB): 19.32, 0.06, 211.33, 33.69, 111.01, 15.63 Prob(Q): 0.75, 0.00, 0.41, 0.66, 0.73, 0.00 Prob(JB): 0.00, 0.97, 0.00, 0.00, 0.00, 0.00 Heteroskedasticity (H): 0.78, 0.86, 2.87, 1.16, 0.08, 0.20 Skew: -0.38, 0.04, -0.69, 0.44, 1.24, 0.16 Prob(H) (two-sided): 0.41, 0.61, 0.00, 0.62, 0.00, 0.00 Kurtosis: 4.66, 2.94, 8.88, 5.25, 6.61, 4.61 Results for equation SwissGDP =================================================================================== coef std err z P>|z| [0.025 0.975] ----------------------------------------------------------------------------------- const 0.2912 0.851 0.342 0.732 -1.376 1.959 L1.SwissGDP 0.2160 0.593 0.364 0.716 -0.947 1.379 L1.Inflation 0.0502 0.377 0.133 0.894 -0.689 0.789 L1.Unemployment 0.2273 1.157 0.196 0.844 -2.041 2.495 L1.Exports 0.0265 0.042 0.629 0.530 -0.056 0.109 L1.Shortspread -0.1068 0.459 -0.233 0.816 -1.006 0.792 L1.Longspread -0.2581 0.549 -0.470 0.638 -1.334 0.818 L2.SwissGDP -0.0129 0.453 -0.028 0.977 -0.900 0.874 L2.Inflation -0.1513 0.376 -0.403 0.687 -0.888 0.585 L2.Unemployment -0.2115 1.189 -0.178 0.859 -2.542 2.119 L2.Exports -0.0023 0.073 -0.031 0.975 -0.145 0.141 L2.Shortspread 0.1188 0.549 0.217 0.829 -0.957 1.194 L2.Longspread 0.3291 0.604 0.545 0.586 -0.855 1.514 beta.EUR/CHF -0.0030 0.135 -0.023 0.982 -0.268 0.262 beta.EUR/CHF_L1 0.0634 0.105 0.602 0.547 -0.143 0.270 beta.EUR/CHF_L2 0.0287 0.100 0.287 0.774 -0.167 0.225 beta.EUR/CHF_L3 -0.0029 0.147 -0.020 0.984 -0.292 0.286 beta.EuroGDP_L1 0.1038 0.632 0.164 0.870 -1.134 1.342 Results for equation Inflation =================================================================================== coef std err z P>|z| [0.025 0.975] ----------------------------------------------------------------------------------- const 0.3652 0.677 0.539 0.590 -0.963 1.693 L1.SwissGDP 0.0388 0.418 0.093 0.926 -0.781 0.859 L1.Inflation -0.2694 0.393 -0.686 0.493 -1.039 0.500 L1.Unemployment 0.4424 1.403 0.315 0.753 -2.308 3.193 L1.Exports 0.0146 0.043 0.342 0.732 -0.069 0.099 L1.Shortspread 0.0660 0.453 0.146 0.884 -0.822 0.954 L1.Longspread -0.1757 0.595 -0.295 0.768 -1.343 0.991 L2.SwissGDP -0.2069 0.575 -0.360 0.719 -1.335 0.921 L2.Inflation 0.1265 0.222 0.571 0.568 -0.308 0.561 L2.Unemployment -0.4376 1.384 -0.316 0.752 -3.150 2.274 L2.Exports 0.0027 0.055 0.050 0.960 -0.105 0.110 L2.Shortspread 0.2494 0.382 0.652 0.514 -0.500 0.999 L2.Longspread -0.0575 0.631 -0.091 0.927 -1.294 1.180 beta.EUR/CHF 0.0039 0.087 0.044 0.965 -0.166 0.174 beta.EUR/CHF_L1 0.0026 0.127 0.021 0.983 -0.246 0.251 beta.EUR/CHF_L2 0.0177 0.109 0.163 0.871 -0.195 0.231 beta.EUR/CHF_L3 0.0306 0.104 0.296 0.768 -0.172 0.234 beta.EuroGDP_L1 0.2990 0.544 0.550 0.582 -0.767 1.365 Results for equation Unemployment =================================================================================== coef std err z P>|z| [0.025 0.975] ----------------------------------------------------------------------------------- const 0.1599 0.148 1.079 0.280 -0.130 0.450 L1.SwissGDP -0.0638 0.091 -0.703 0.482 -0.242 0.114 L1.Inflation 0.0056 0.108 0.052 0.959 -0.206 0.217 L1.Unemployment 1.7436 0.185 9.450 0.000 1.382 2.105 L1.Exports 0.0018 0.011 0.167 0.867 -0.019 0.022 L1.Shortspread 0.0004 0.068 0.006 0.995 -0.132 0.133 L1.Longspread 0.0164 0.142 0.115 0.908 -0.262 0.294 L2.SwissGDP -0.0145 0.131 -0.111 0.912 -0.271 0.242 L2.Inflation 0.0060 0.078 0.077 0.939 -0.147 0.159 L2.Unemployment -0.7866 0.191 -4.122 0.000 -1.161 -0.413 L2.Exports 0.0034 0.014 0.247 0.805 -0.023 0.030 L2.Shortspread -0.0339 0.094 -0.362 0.718 -0.217 0.150 L2.Longspread -0.0070 0.134 -0.052 0.959 -0.271 0.257 beta.EUR/CHF -0.0009 0.015 -0.065 0.948 -0.029 0.028 beta.EUR/CHF_L1 -0.0027 0.014 -0.195 0.846 -0.029 0.024 beta.EUR/CHF_L2 0.0017 0.019 0.092 0.927 -0.035 0.039 beta.EUR/CHF_L3 0.0046 0.016 0.296 0.767 -0.026 0.035 beta.EuroGDP_L1 -0.0270 0.141 -0.192 0.848 -0.303 0.249 Results for equation Exports =================================================================================== coef std err z P>|z| [0.025 0.975] ----------------------------------------------------------------------------------- const 0.2117 8.834 0.024 0.981 -17.103 17.527 L1.SwissGDP 1.4168 7.507 0.189 0.850 -13.297 16.131 L1.Inflation -0.1542 3.754 -0.041 0.967 -7.512 7.203 L1.Unemployment 4.2236 15.231 0.277 0.782 -25.629 34.076 L1.Exports -0.2334 0.328 -0.711 0.477 -0.877 0.410 L1.Shortspread 0.0022 3.357 0.001 0.999 -6.577 6.581 L1.Longspread -1.9147 4.632 -0.413 0.679 -10.993 7.164 L2.SwissGDP -0.0285 5.307 -0.005 0.996 -10.430 10.373 L2.Inflation -1.3139 3.632 -0.362 0.718 -8.432 5.804 L2.Unemployment -4.0944 13.846 -0.296 0.767 -31.232 23.043 L2.Exports -0.1999 0.380 -0.527 0.598 -0.944 0.544 L2.Shortspread 0.9305 4.161 0.224 0.823 -7.225 9.086 L2.Longspread 2.1317 4.209 0.507 0.613 -6.117 10.380 beta.EUR/CHF 0.0228 1.173 0.019 0.985 -2.277 2.323 beta.EUR/CHF_L1 0.1065 1.216 0.088 0.930 -2.278 2.491 beta.EUR/CHF_L2 0.1484 0.769 0.193 0.847 -1.358 1.655 beta.EUR/CHF_L3 -0.1000 0.723 -0.138 0.890 -1.517 1.317 beta.EuroGDP_L1 1.7469 4.490 0.389 0.697 -7.053 10.546 Results for equation Shortspread =================================================================================== coef std err z P>|z| [0.025 0.975] ----------------------------------------------------------------------------------- const 0.1305 1.601 0.082 0.935 -3.008 3.269 L1.SwissGDP -0.0318 0.960 -0.033 0.974 -1.914 1.851 L1.Inflation 0.0794 1.156 0.069 0.945 -2.187 2.346 L1.Unemployment 0.5326 2.243 0.237 0.812 -3.864 4.929 L1.Exports -0.0027 0.153 -0.018 0.986 -0.303 0.297 L1.Shortspread 0.3506 0.523 0.671 0.503 -0.674 1.375 L1.Longspread -0.0849 1.719 -0.049 0.961 -3.454 3.285 L2.SwissGDP 0.5461 1.114 0.490 0.624 -1.637 2.729 L2.Inflation 0.1820 1.366 0.133 0.894 -2.495 2.859 L2.Unemployment -0.5416 2.317 -0.234 0.815 -5.082 3.999 L2.Exports -0.0243 0.118 -0.205 0.837 -0.256 0.207 L2.Shortspread 0.0617 0.583 0.106 0.916 -1.081 1.204 L2.Longspread 0.0132 1.674 0.008 0.994 -3.269 3.295 beta.EUR/CHF -0.0138 0.183 -0.075 0.940 -0.372 0.345 beta.EUR/CHF_L1 -0.0377 0.225 -0.168 0.867 -0.479 0.403 beta.EUR/CHF_L2 -0.0057 0.186 -0.030 0.976 -0.369 0.358 beta.EUR/CHF_L3 -0.0228 0.217 -0.105 0.916 -0.448 0.402 beta.EuroGDP_L1 -0.2505 0.822 -0.305 0.761 -1.861 1.360 Results for equation Longspread =================================================================================== coef std err z P>|z| [0.025 0.975] ----------------------------------------------------------------------------------- const 0.0375 0.840 0.045 0.964 -1.609 1.684 L1.SwissGDP -0.0971 0.480 -0.202 0.840 -1.038 0.844 L1.Inflation -0.1951 0.422 -0.463 0.644 -1.022 0.632 L1.Unemployment -0.0719 1.781 -0.040 0.968 -3.562 3.418 L1.Exports 0.0058 0.048 0.122 0.903 -0.087 0.099 L1.Shortspread 0.2619 0.321 0.816 0.415 -0.367 0.891 L1.Longspread 1.1997 0.611 1.962 0.050 0.001 2.398 L2.SwissGDP 0.0101 0.593 0.017 0.986 -1.151 1.171 L2.Inflation -0.0314 0.320 -0.098 0.922 -0.658 0.595 L2.Unemployment 0.1315 1.703 0.077 0.938 -3.205 3.468 L2.Exports -0.0018 0.074 -0.024 0.981 -0.147 0.143 L2.Shortspread -0.2239 0.300 -0.747 0.455 -0.811 0.363 L2.Longspread -0.3825 0.557 -0.687 0.492 -1.474 0.709 beta.EUR/CHF 0.0040 0.159 0.025 0.980 -0.308 0.316 beta.EUR/CHF_L1 -0.0169 0.154 -0.110 0.913 -0.319 0.285 beta.EUR/CHF_L2 -0.0314 0.077 -0.406 0.684 -0.183 0.120 beta.EUR/CHF_L3 0.0078 0.141 0.055 0.956 -0.269 0.285 beta.EuroGDP_L1 0.0081 0.590 0.014 0.989 -1.147 1.164 Error covariance matrix ===================================================================================================== coef std err z P>|z| [0.025 0.975] ----------------------------------------------------------------------------------------------------- sqrt.var.SwissGDP 0.5079 0.124 4.107 0.000 0.265 0.750 sqrt.cov.SwissGDP.Inflation 0.0564 0.171 0.330 0.742 -0.279 0.392 sqrt.var.Inflation 0.4902 0.125 3.935 0.000 0.246 0.734 sqrt.cov.SwissGDP.Unemployment -0.0192 0.043 -0.452 0.651 -0.103 0.064 sqrt.cov.Inflation.Unemployment 0.0051 0.056 0.092 0.926 -0.104 0.114 sqrt.var.Unemployment 0.0825 0.017 4.847 0.000 0.049 0.116 sqrt.cov.SwissGDP.Exports 1.4706 2.281 0.645 0.519 -3.000 5.941 sqrt.cov.Inflation.Exports 0.5989 2.527 0.237 0.813 -4.354 5.551 sqrt.cov.Unemployment.Exports 0.1911 2.621 0.073 0.942 -4.946 5.329 sqrt.var.Exports 3.9067 1.106 3.533 0.000 1.739 6.074 sqrt.cov.SwissGDP.Shortspread -0.0485 0.680 -0.071 0.943 -1.382 1.285 sqrt.cov.Inflation.Shortspread 0.0111 0.426 0.026 0.979 -0.825 0.847 sqrt.cov.Unemployment.Shortspread -0.0115 0.719 -0.016 0.987 -1.420 1.397 sqrt.cov.Exports.Shortspread 0.0584 0.337 0.173 0.863 -0.603 0.719 sqrt.var.Shortspread 0.7694 0.278 2.767 0.006 0.224 1.314 sqrt.cov.SwissGDP.Longspread -0.0693 0.222 -0.313 0.754 -0.503 0.365 sqrt.cov.Inflation.Longspread -0.0595 0.168 -0.354 0.723 -0.389 0.270 sqrt.cov.Unemployment.Longspread -0.0262 0.376 -0.070 0.945 -0.764 0.711 sqrt.cov.Exports.Longspread -0.0238 0.242 -0.098 0.922 -0.498 0.451 sqrt.cov.Shortspread.Longspread -0.0599 0.189 -0.316 0.752 -0.431 0.311 sqrt.var.Longspread 0.3893 0.135 2.883 0.004 0.125 0.654 ===================================================================================================== Warnings: [1] Covariance matrix calculated using the outer product of gradients (complex-step).

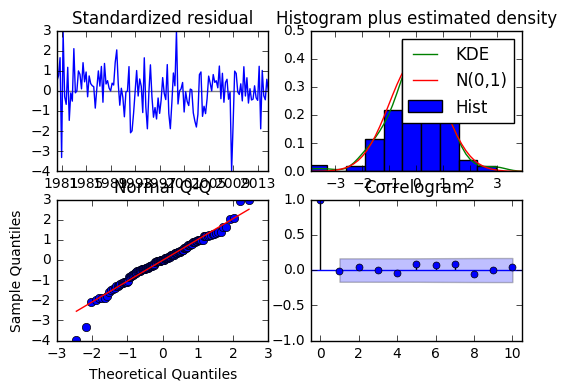

The residual diagnostics plot looks quite similar to the one of the ARMAX model.

Also the VARMAX model predicts the GDP to be considerably lower.

# In-sample one-step-ahead predictions, and out-of-sample forecasts

nforecast = 11

predict = res.get_prediction(end=mod.nobs + nforecast, exog = fx)

""" idx = np.arange(len(predict.predicted_mean)) """

predict_ci90 = predict.conf_int(alpha=0.1)

predict_ci60 = predict.conf_int(alpha=0.4)

predict_ci30 = predict.conf_int(alpha=0.7)

fidx = predict_ci90.index

predict_ci90.iloc[138,:] = SwissGDP.iloc[138,:].values

predict_ci60.iloc[138,:] = SwissGDP.iloc[138,:].values

predict_ci30.iloc[138,:] = SwissGDP.iloc[138,:].values

# Graph

fig5, ax = plt.subplots(figsize=(12,6))

ax.grid()

ax.plot(idx,SwissGDP,'k',label='', alpha=0.7, linewidth=0.75)

ax.plot(idx,SwissGDP,'k.', label='Actual Values', alpha=0.7, linewidth=0.75)

# Plot

ax.plot( predict.predicted_mean[:-nforecast-1][['SwissGDP']], 'gray',label='In Sample Prediction')

ax.plot(fidx[-nforecast-1:], predict.predicted_mean[-nforecast-1:][['SwissGDP']], 'k--', linestyle='--', linewidth=1.5,label='Out of Sample Prediction')

ax.fill_between(fidx[-nforecast-2:], predict_ci90.iloc[-nforecast-2:, 0], predict_ci90.iloc[-nforecast-2:, 6], alpha=0.15, label= '')

ax.fill_between(fidx[-nforecast-2:], predict_ci60.iloc[-nforecast-2:, 0], predict_ci60.iloc[-nforecast-2:, 6], alpha=0.15, label= '')

ax.fill_between(fidx[-nforecast-2:], predict_ci30.iloc[-nforecast-2:, 0], predict_ci30.iloc[-nforecast-2:, 6], alpha=0.15, label= '')

# Retrieve and also plot the NBER recession indicators

rec = DataReader('USREC', 'fred', start=idx[0], end=idx[138])

recr = rec.iloc[0:413:3,0]

ylim = ax.get_ylim()

ax.fill_between(recr.index, ylim[0], ylim[1], recr, facecolor='k', alpha=0.1);

ax.legend()

ax.set_xlim(730000.0, 736603.0)

ax.set(title='VARMAX - Forecasting Swiss GDP');

plt.show(fig5)

Comments You need to have a GitHub Account to comment!

Post comment